By Wells Fargo Advisors

For most investors, the key to success is simple: Buy low and sell high. But how often have you seen this scenario played out? (You may have done it yourself.)

When the market is up, an investor feels good and buys stocks.

When the market is down, that same investor gets scared and sells.

Although reacting like this may feel instinctively right at the time, buying high and selling low is unlikely to result in a profit.

Why do investors do this? The reason may have a lot to do with us making investment choices the same way we do many important decisions: using both our heads and our hearts (i.e., logic and emotion). When there’s market volatility—including both market highs and market lows—our emotions tend to take over and we may make illogical choices going against our best interests.

Rather than falling victim to the potential perils of emotional investing, you may want to be completely logical: get into the market when it’s down and out when it’s up. This is known as “market timing.” While this approach sounds rational, the problem is it’s extremely difficult, even for experienced investors, to do consistently. There’s an old saying: “No one rings a bell” when the market reaches the top of a peak or the bottom of a trough. Translated, that means anyone attempting to time the market finds it difficult to know exactly when to make their move.

For example, if you think the market has reached a peak and get out and then share prices keep rising, you’ll miss out on the additional profits you could have made by waiting. And after you get out, how do you know when to get back in? If you act too quickly, you’ll forego better bargains as prices continue to fall. If you wait too long, you may sacrifice the chance to fully benefit from a market rally.

Give dollar cost averaging a look

To avoid the potential problems of emotional investing and market timing, consider a strategy called “dollar cost averaging.”

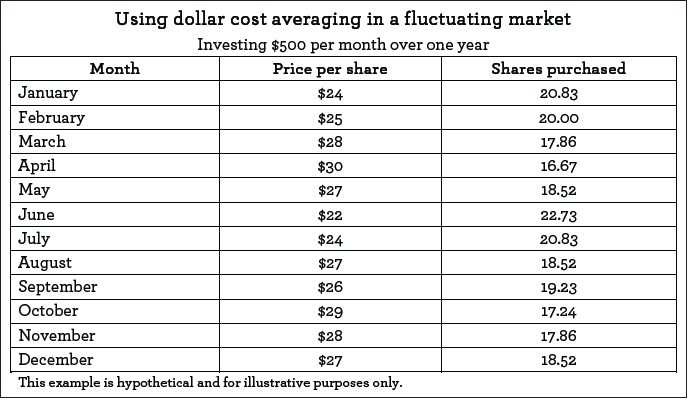

Dollar cost averaging is the practice of putting a set amount into a particular investment on a regular basis (weekly, monthly, quarterly, etc.) no matter what’s going on in the market. For example, you could invest $500 each month. In a fluctuating market, this practice lets you purchase:

Additional shares when prices are low

Fewer shares when prices increase

As shown in the table above, if the price is $24 per share, you’d buy 20.83 shares (keep in mind mutual funds let you purchase fractional shares). If it rises to $30, you would buy only 16.67 shares.

In a fluctuating market, dollar cost averaging will result in an average cost per share that’s less than the average market price per share. The average market price per share in the table (the sum of the market prices [$317] divided by the number of purchases [12]) is $26.42. However, the average price per share (the total invested [$6,000] divided by the number of shares purchased [228.81]) is only $26.22.

While you’re mulling dollar cost averaging’s potential merits, consider this: You may well be using the strategy already. If you participate in an employer-sponsored retirement plan, such as a 401(k) or 403(b), and contribute the same amount each payday, you’re using dollar cost averaging.

Get help for when the going gets tough

One of dollar cost averaging’s challenges is you have to stick with the strategy even when the market declines, and that can be difficult (see our previous discussion about emotional investing). However, during times like these, dollar cost averaging can be most useful by letting you purchase shares at lower prices.

Because dollar cost averaging can be simultaneously more difficult and advantageous when the going gets toughest, consider turning to a professional financial advisor for help. He or she should offer a voice a reason during these periods as you grapple with whether to adhere to the strategy.

Like any investment strategy, dollar cost averaging doesn’t guarantee a profit or protect against loss in a declining market. Because dollar cost averaging requires continuous investment regardless of fluctuating prices, you should consider your financial and emotional ability to continue the program through both rising and declining markets.

This article was written by/for Wells Fargo Advisors and provided courtesy of Whitney McDaniel, CFP®, Financial Advisor in Beaufort, SC at (843) 524-1114

Investments in securities and insurance products are: NOT FDIC-INSURED/NOT BANK-GUARANTEED/MAY LOSE VALUE

Wells Fargo Advisors is a trade name used by Wells Fargo Clearing Services, LLC, Member SIPC, a registered broker-dealer and non-bank affiliate of Wells Fargo & Company.

© 2018-2019 Wells Fargo Clearing Services, LLC. All rights reserved.